Ask Not Wen Moon–Ask Why Moon

2021 was a banner year for crypto: hundreds of projects launched, thousands of new developers and over 100m new users entered the space, total crypto market cap increased by a trillion USD, DeFi total value locked 4x’d to ~$250B, NFT sales broke records and garnered an SNL feature, Tom Brady & Gisele backed FTX spurring a wave of tastemaker interest in crypto, pleasrDAO rescued the Wu Tang Clan album, ConstitutionDAO almost bought the constitution, and more.

Yet, we still hear the same questions from people new to the space: WTH is happening in crypto? Is it a currency or investment or a new internet? What are the hot new tokens and NFTs? Wen Moon?

The better question is actually: Why Moon? Why is crypto/web3 happening? Why now? Beyond the token market caps that tend to put $$ in people’s eyes, why does it matter?

While arguably a Sisyphean task, we tried to answer these questions in a few pages. This will feel simplistic to anyone deep in the space, but our hope is that by providing a broad overview of crypto in its historical context and a decent mental model for the ecosystem, more people—users, developers, operators, and founders—will dive in. We also hope it sheds some light on why Sequoia has conviction that crypto is one of the most important platform shifts of our time.

Why crypto is happening and why it matters (the 30,000 foot view)

Money is about trust. Many people on our planet enjoy trust in their money and financial systems. We trust our central banks not to devalue our currency overnight. We trust our governments to avoid hyperinflation so our money retains purchasing power. We trust banks to secure our money and not loan it recklessly, and private companies to help us safely use our money for commerce and other financial services. We pay for the privilege of this trust in taxes and fees to financial services companies (a multi-trillion dollar industry). This foundation of trust has been an essential bedrock of our economic progress over the last few centuries.

Yet, many do not enjoy this level of trust in their financial systems, if they can access them at all. This is true even in some of the most prosperous and populous countries. Recent events, especially the Great Financial Crisis of ‘08-09, eroded trust even in the US. Global monetary stimulus in response to COVID has many questioning again whether their trust is well‐placed.

It is unlikely a coincidence that the Bitcoin whitepaper which ignited the crypto industry was published October 31, 2008, just six weeks after Lehman Brothers collapsed in the Great Financial Crisis. Titled “Bitcoin: A Peer‐to‐Peer Electronic Cash System,” it described the solution to a holy‐grail problem in cryptography: using a distributed network to validate the authenticity of a digital file. This introduced a new phenomenon on the Internet: verifiable scarcity, and enabled the direct transfer of value online without intermediaries. To exchange Bitcoin, all we need is internet access and trust in Bitcoin’s open source code. Just as billions now trust the Internet for the global free exchange of information, 220M and counting now trust a blockchain for the global free exchange of value.

Viewed in historical context, “internet money” can be seen as a natural evolution of our financial system. The history of money is a story of progressive abstraction for the sake of convenience (barter economy to metal coins to paper money etc.) Today, most of the money flying around the world is already digital, and we true up the paper as an afterthought as we once did with gold. But we pay a great cost for the inefficiencies of this analog system with its fragmented jurisdictions, myriad intermediaries, and long settlement delays. Why wouldn’t we move to internet-native money movement rails? Isn’t this the next step in a journey arguably started by PayPal, Stripe, Square and others?

While it seems Bitcoin was intended to solve a payments problem, inventions rarely go as their inventors planned. As demand for Bitcoin grew, its price and transaction fees increased, making it more useful for many as an investment vehicle (or store of value) than a payment mechanism (medium of exchange). Most interestingly, new inventors built on the concepts of Bitcoin in new ways. Ethereum’s contribution was using a distributed ledger not just for currency but for computation.

Blockchains as decentralized computing platforms captured developers’ imaginations. Their aims are wide‐ranging but can be roughly characterized as trying to bring about better money and a better internet.

- Better money: money free from arbitrary monetary policy, censorship and surveillance, and financial systems that are more trustworthy, accessible, efficient and cheaper

- Better internet: applications in which users own their data, rather than rent access from a given platform, creators are better rewarded, and communities govern them; digital goods (NFTs) that are more liquid, portable across platforms, better suited to manage digital rights

While these are the goals, we still have a long way to go. Some point to crypto’s shortcomings as evidence the entire effort is a scam, but this misses the point. Historically, when technological innovation has led to financial innovation ahead of regulation, we have seen world-changing innovation, then mania, fraud, a crash, a regulatory framework and then a slow build toward lasting value (see: early stock markets of 1600s Amsterdam). Crypto appears no different. There are tokens of dubious quality. There are pockets of over-hype. But as with all other technology revolutions, there will also be enduring companies created in this time.

The Great Transformation

Crypto will transform value on the Internet, and in doing so, the Internet itself. Blockchains will rewrite the way we own, sell, buy, trade, exchange and reward. As software saturates our world, crypto (software money) will saturate money—and everything we do with it. Blockchain’s inherent properties—instant value transfer, verifiable scarcity, and user‐ownership—could restructure trillions of market cap across payments, finance, gaming, content, social networks and more.

- Digital currencies are fundamentally useful to 220M people and counting, whether as capped‐supply inflation hedges, censorship‐resistant stores of value, borderless mediums of exchange and/or investment vehicles. This has created a new asset class.

- This new asset class is creating a market for financial services, both centralized and decentralized (DeFi). As with any asset class, owners want to be able to buy, hold, sell, trade, lend, hedge, swap, fractionalize, insure and more. With crypto, they also want to do it freely across borders and time zones, 24/7. This is likely to be expansionary to current financial systems, creating more consumer choice.

- The rise of crypto necessitates a new crypto stack. From core infrastructure to developer tools, some of the traditional stack will translate and some won’t. Custody, nodes, fiat<>crypto on/off ramps and both on and off-chain data are just a few areas of the emerging crypto stack. In this era, value may accrue to new layers. In traditional software, more value accrued to the application layer (Google ~$2T market cap, TCP/IP/SMTP arguably $0) whereas in crypto, core protocols are monetizable via tokens (BTC+ETH ~$2T market cap vs. crypto apps ~$200B so far).

- Blockchains enable more than digital assets—they also enable digital goods (NFTs) and decentralized applications (web3). While these areas are exploding in trading volumes, user interest and developer energy, they are still in their earliest innings. Web3 holds tremendous potential to use blockchains to reshape internet services around principles of user ownership, creator rewards, and community governance (e.g., DAOs).

- However, regulatory frameworks are still being clarified, so founders will need to thoughtfully navigate uncharted waters.

Mental Model for Crypto

It can be helpful to organize crypto along two dimensions: space and time.

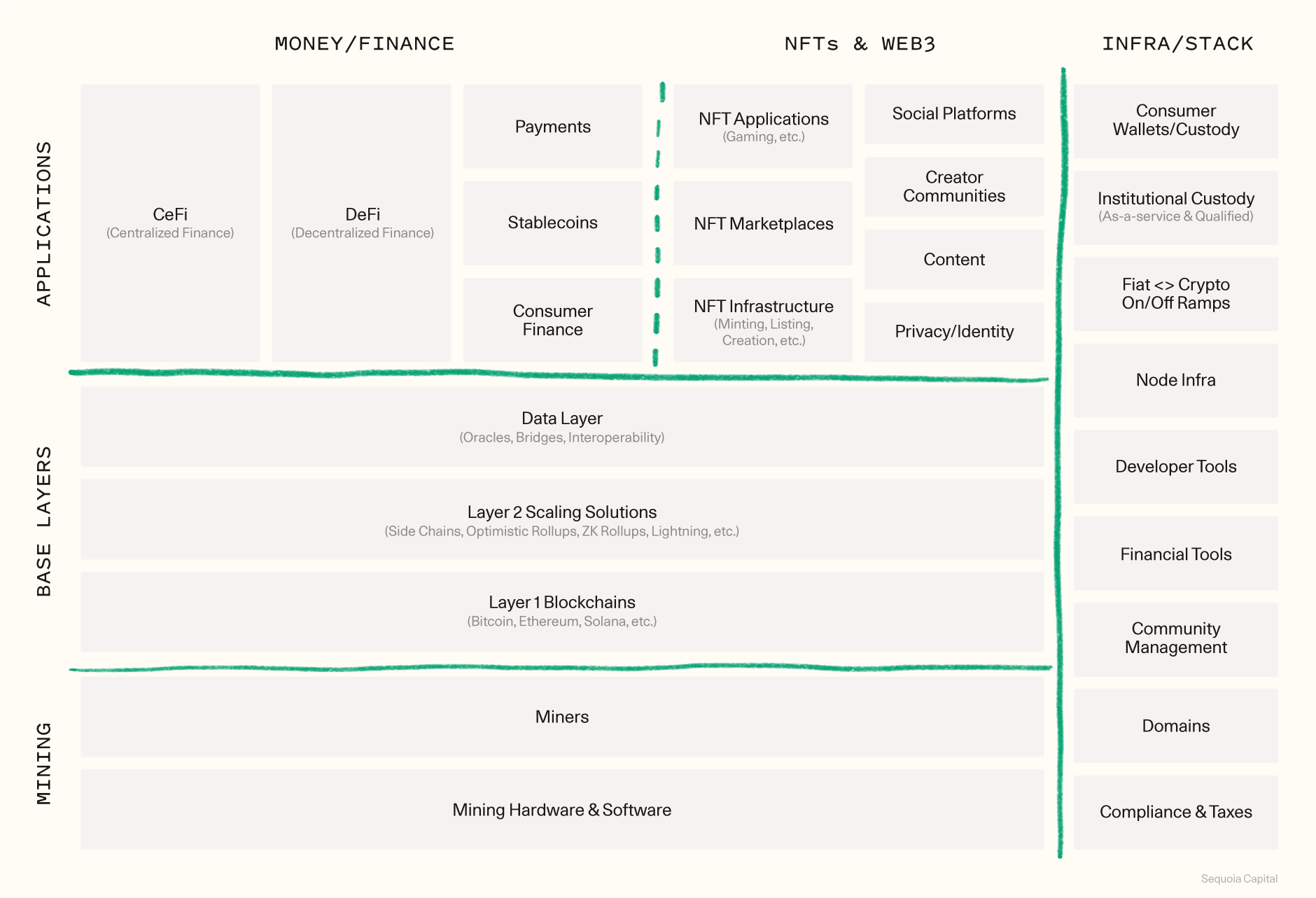

Space: Below is a map of the crypto ecosystem. It’s organized like a typical stack from hardware at the bottom to applications at the top, with the infrastructure to build and access it on the right. Before you get out your pitchforks, we know this is imperfect. Crypto doesn’t fit neatly into little boxes. Many of these categories overlap and crypto is constantly changing. But, it’s not a terrible starting point. We welcome input from the community.

We’ll share our deep dives into each of these areas in future posts.

Time: Here is a framework for when certain areas of opportunity may mature, inspired by a typical new technology adoption S-curve. This is again imperfect—building is happening simultaneously, phases are overlapping and interact in feedback loops. This is also not a replay of every local maxima and minima over the past decade. Instead, this is an attempt to zoom way out and imagine how we might move from millions to billions of crypto users.

- Phase 1: Isolation. Crypto as an island, disconnected from the non‐crypto world. Core protocols are built out (think TCP/IP for internet, and layer 1 blockchains like Bitcoin, Ethereum and Solana for crypto). Protocols are inextricable from their native coins. A variety of coins creates demand for exchanges and additional financial services. Most incumbents lack the tech and regulatory appetite to serve this demand, allowing crypto‐natives to fill the void. Crypto‐native analogs of every financial service arise roughly in their historical order: currency, foreign exchange, lending, derivatives, insurance, options, ETFs, etc.

- Phase 2: Connectivity. Bridging the crypto and non‐crypto worlds. The non‐crypto world sees value in crypto and builds/buys the infrastructure to access it. Custody/wallets, crypto<>fiat on/off ramps, data feeds, blockchain‐specific infrastructure and developer tools grow exponentially in this time. New use cases from NFT art communities to gaming to web3 social networks draw in new users. As the mass-market starts to engage in crypto, competitive pressure dramatically simplifies the user experience and lowers barriers to access. The number of users and developers with access to crypto increases by 10-100x over this next decade. We’d argue we are just starting Phase 2.

- Phase 3: Maturation. Fusion of crypto and non‐crypto worlds so they are no longer distinct. Like mobile, once crypto access is sufficiently ubiquitous, applications will have the foundation they need to reach their full potential. They will cross the chasm from crypto‐niche to commonplace. To be clear, founders are already building across consumer finance, DeFi, NFT, web3 and more, but only a few hundred million people and institutions have the tools to access them. As access spreads, applications will see an order of magnitude increase in user engagement.

Looking Forward

Crypto is still in its early innings. Though it is rife with volatility, it’s also ripe with innovation. To dismiss crypto as purely speculative is to ignore the history that every financial innovation has had its misusers and to miss the tremendous potential crypto holds to create better financial systems. To dismiss crypto as too slow, expensive, or confusing to ever be useful is like dismissing the Internet in its dial-up phase. While criticisms of crypto’s user experience, cost, speed or environmental impact are all valid, these aren’t doomsday signals for the movement—they are opportunities to build. The bottom line is: billions of people want a better financial system and a better internet and a new generation of developers is motivated to build that for them.

Sequoia Crypto

Like all other waves of technology, Sequoia’s mission is to partner with the most daring founders in crypto and help them build something legendary. We’re proud partners of Sam at FTX, Jack at Square now Block, Michael at Fireblocks, Uri at Starkware, Elena at Iron Fish, Nader at DeSo, Vlad at Robinhood, and a dozen other seed-stage companies still in stealth. Because we believe crypto will impact every industry, crypto is a firm-wide focus that includes myself (FTX, Fireblocks), Shaun Maguire (DeSo, ParallelFi, Iron Fish, Faraway, Strips, and more seeds in stealth), Alfred Lin (FTX), Mike Vernal (Starkware), Ravi Gupta (Fireblocks), Roelof Botha (Square now Block), Andrew Reed (Robinhood), Stephanie Zhan (stealth seed, Brud acquired by Dapper Labs) and more. Sequoia has been investing in crypto since 2017 and backs founders pre-seed and beyond in equity and tokens.

If you are a founder building in crypto/web3, we’d love to meet you. Feel free to email us, ping us at crypto@sequoiacap.com or DM us on Twitter or Telegram.

PS: Thank you to my Sequoia teammates (Andrew Reed, Alfred Lin, Daniel Chen, Pat Grady, and Shaun Maguire) as well as Ramnik Arora of FTX, Elena Nadolinski of Iron Fish and Bryan Pellegrino of LayerZero for reviewing drafts. Thank you as well to all the builders we’ve spent time with over the years who helped inform our perspectives.